Potential of carbon emission reduction investments in plantations on tropical peatland

Some considerations based on our experience and insights:

We propose that full restoration of plantations, rewetting the land to allow peat swamp forest to return and drastically reduce carbon emissions, could offer specific benefits to both plantation companies and investors (see our Q&A #2), even though this approach may take time to develop and is not widely considered now.

For companies managing plantations on peatland, restoration would reduce their overall carbon emissions (of which the bulk is often produced by peat decomposition, dwarfing other emissions), while co-investment by others would reduce opportunity costs (lost production) and the costs of restoration interventions. If restoration involves areas that have low productivity due to frequent flooding, at present or in the near future, the opportunity cost to the company is further limited. This 'point of no return' is now being reached over millions of hectares of peatland across Southeast Asia, and companies will need to start thinking harder about a transition to a non-drainage future for their lands before they flood permanently. Eventually, there may be a pathway for them to directly benefit from carbon credits from their concessions on peat, even though this is currently not possible.

For investors, a major upside to working with large plantation companies would be that these companies have a well-established mandate to manage concession land, and substantial operational and monitoring capacity on the ground, ensuring they can deliver restoration as planned which can sometimes not be said of all organizations already active in restoration. Community issues are often less of a concern in thinly populated plantation landscapes. Fires have largely been eliminated from many plantations in recent years due to substantial monitoring and fire extinguishing capacity combined with stricter enforcement by governments. If there are policy issues standing in the way of taking designated 'productive' land out of production (with the note that production in some cases is already minimal or absent), the largest plantation companies may have the political clout to find solutions. In summary, many of the uncertainties that are now stopping investors from stepping into peatland restoration in Southeast Asia are much reduced on some plantation lands.

One main type of concerns around restoration on plantation land is that of additionality and leakage. In principle, an organization that is responsible for causing emissions through peatland deforestation and drainage can not financially benefit from taking credit for undoing some of that damage. However this may be different if a new independent entity is established to control the restoration execution and benefits, separated from the original plantation company. Meanwhile, uncertainties around leakage may be mitigated by public company pledges to not expand operations into forest and peatland areas, as several large players have announced over the last 10 years.

Clearly, most peatlands now utilized for plantations can not be restored in the near future; financial dependencies on continued production are large and there is global demand for the products. However there are areas where other factors may outweigh these short term financial interests. Identifying potential projects will likely best start by considering such areas:

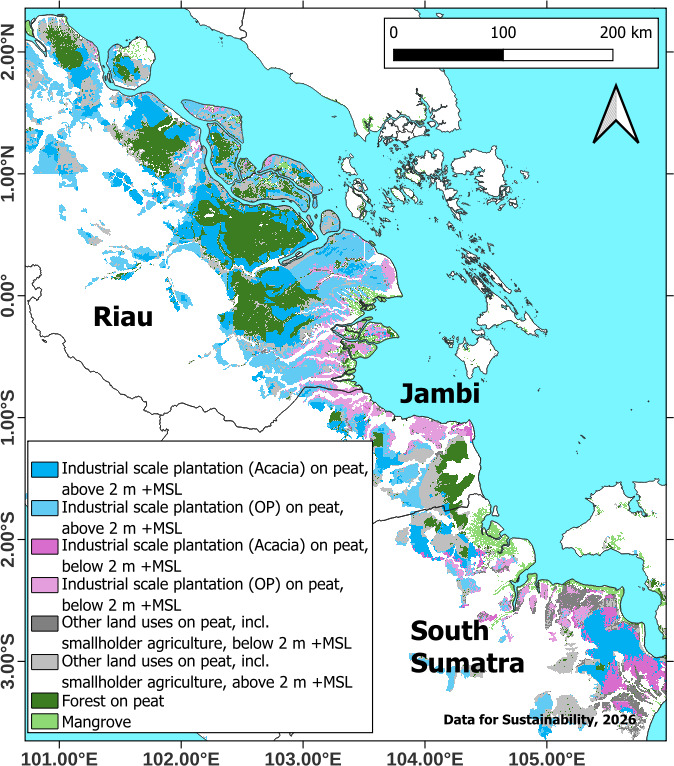

- Unproductive land, currently or in the near future. Extensive coastal peatland areas have already subsided to a degree, often by several metres over a few decades, that brings land surfaces near the tidal range where flooding becomes frequent and inevitable (see Figure 1, and our Q&A #1). Such areas already have limited crop yields or none at all, while water management aiming to reduce flooding is costly and generally ineffective. Companies could incur less cost by giving up such land for restoration, compared to continuing to invest in unproductive crop systems, while occasional flooding would benefit rapid restoration of flood tolerant forest types. This could include mangroves where tidal intrusion of sea water already occurs. The carbon capture in such new forest biomass could be substantial and add to the volume of creditable carbon stock. In fact, some wetland forest restoration projects may yield forest that can be commercially harvested under a sustainable 'paludiculture' model, at long rotation cycles and without degrading the surface hydrology and ecosystem integrity; this would further reduce nett restoration cost and also political opposition to 'giving up production land'.

- Buffer zones along conservation forest within or adjoining plantation concessions. Such forest near plantations is now often in poor condition (our Q&A #4), generating carbon emission while losing biodiversity, as plantation drainage systems usually are not designed to maintain higher water levels in peripheral areas. The lateral impact of plantation drainage into peat swamp forest has been shown to be substantial over a distance of at least 1 km from perimeter canals. Buffer zones along plantation perimeters could therefore be 1 km wide, and consist of two steps: the 500 m along the forest edge should be fully rewetted and support regrowth of new peat swamp forest, while the 500 m on the plantation side could have somewhat lower water levels that still support crop production, but raised relative to the plantation water level. We estimate that many hundreds of kilometres of plantation boundaries along remaining forest or otherwise protected peatland are in need of buffer zones, yielding tens of thousands of hectares to be restored. Carbon credit may be obtained for rewetting not only the plantation but also the formerly dried-out forest.

- Land already allocated for restoration, by Government or by companies under voluntary agreements. Such restoration may not be considered 'additional' and therefore not yield carbon credits, but it may fit into a portfolio of supported activities especially where these allocated areas are adjoining to other restoration areas (unproductive or buffer zones) and can add to ecosystem values at the landscape scale.

- Combination Landscapes can be identified where at least 2 of the 3 cases mentioned above exist in close proximity. Where a concession would already be partly unproductive due to flooding, while it also contains or adjoins conservation forest in need of buffer zones, there could be cases where converting the remaining productive land to restoration produces large units of restoration peatland with reduced technical challenges in terms of maintaining different water depths over short distances.

Figure 1. Map of industrial plantations on peatland in Sumatra, in relation to elevation. Notes: 1. land below 2 m +MSL, flood issues are increasingly problematic and productivity is dropping or already zero. 2. land above 2 m +MSL, potentially productive.

Selected Further Reading (D4S Publications)

- Subsidence and carbon loss in drained tropical peatlands

- Extent of industrial plantations on Southeast Asian peatlands in 2010 with analysis of historical expansion and future projections

- Flooding projections from elevation and subsidence models for oil palm plantations in the Rajang Delta peatlands, Sarawak, Malaysia

- Hydrological and economic effects of oil palm cultivation in Indonesian peatlands

- Benefits of tropical peatland rewetting for subsidence reduction and forest regrowth: Results from a large-scale restoration trial